While Americans often exhibit a strong appetite for financing, U.S. credit card debt trended downward during the coronavirus pandemic. With the CARES Act providing enhanced unemployment benefits and periodic stimulus checks, unprecedented fiscal support negated consumers’ need for credit card debt.

Moreover, while COVID-19 upended global markets, disrupted economic activity, and dislocated the U.S. labor market, households’ finances were sheltered from the storm.

For context, our study on the Average Credit Score in America of July 2025 also provides essential details on the developments that contributed to record-high U.S. creditworthiness.

With accuracy and accountability in mind, we pride ourselves on presenting you with the latest information from the most reliable sources. We carefully select data from the largest credit reporting agencies – like FICO, Equifax, Experian, and TransUnion. In addition, we augment our studies with relevant data from the U.S. government, the U.S. Federal Reserve (Fed), the Consumer Financial Protection Bureau (CFPB), and other reputable research institutions.

Moreover, our editorial team carefully vets all of the findings, and sources are present throughout the study.

National Statistics:

Americans’ average credit card balance is $5,525 — a decrease of 6% year-over-year (YoY).

Americans’ average revolving utilization ratio is 25% — a decrease of 4% YoY.

Total outstanding credit card loans made by FDIC-insured institutions as of Q3 2021 were $806 billion — an increase of 1% YoY.

By Age:

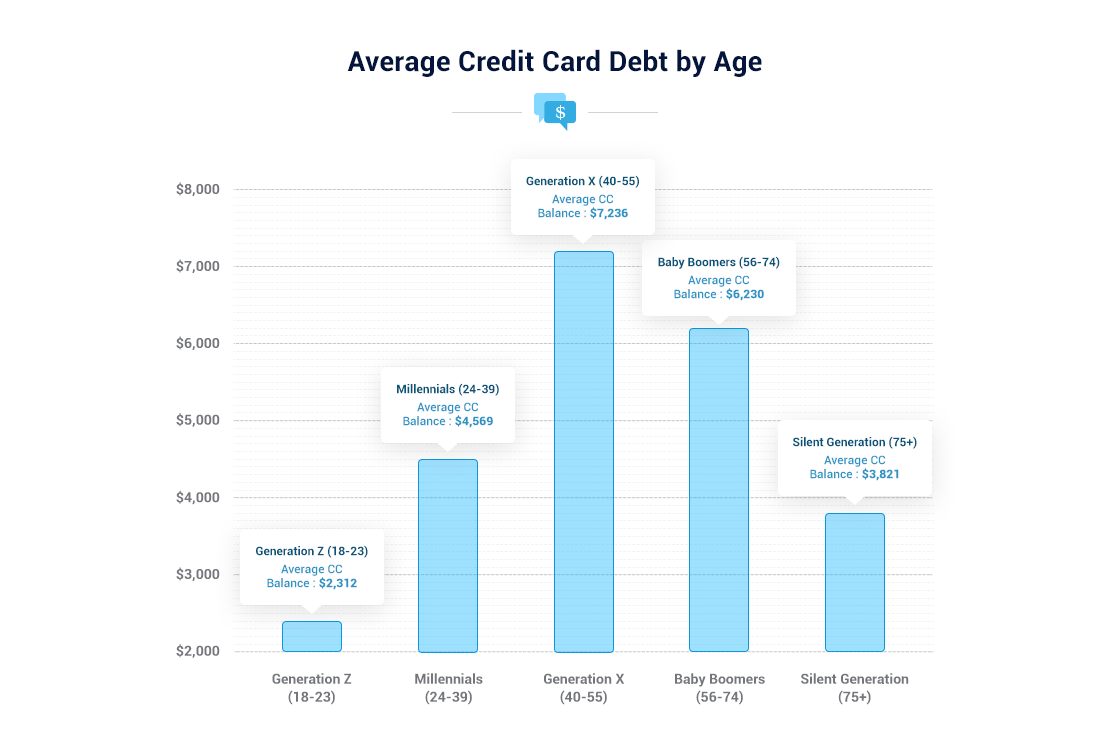

Generation X ($7,236) has the highest average credit card balance, while Generation Z ($2,312) has the lowest average credit card balance.

Generation Z (31.1%) has the highest revolving utilization ratio, while the Silent Generation (12.6%) has the lowest revolving utilization ratio.

Baby Boomers (3.4) own the highest number of credit cards, while Generation Z (1.7) owns the lowest number of credit cards.

Credit card borrowers aged 18 to 39 (Gen Z and Millennials) have the highest delinquency rates across all age groups.

By Income:

There is a strong positive correlation between Americans’ median annual incomes and their average credit card debt.

Americans with median annual incomes of $16,290 or less have $3,830 in average credit card debt. Conversely, Americans with median annual incomes of $290,160 or more have $12,600 in average credit card debt.

By Gender:

American men carry average credit card debt of $7,407, while American women carry average credit card debt of $5,245.

By Race:

White Americans ($6,940) have the highest average credit card debt, while Black Americans ($3,940) have the lowest average credit card debt.

By State:

Millennials in Alaska ($5,388), Washington, D.C. ($5,118), and New Jersey ($5,034) have the highest average credit card debt, while Millennials in Mississippi ($3,724), Kentucky ($3,826), and Vermont ($3,843) have the lowest average credit card debt.

There is a strong correlation (0.74) between Millennials’ average credit card debt service coverage ratios (DSCRs) and their average FICO Scores.

Millennials in Massachusetts (18.7), Washington, D.C. (17.6), and Connecticut (16.5) have the highest DSCRs. And unsurprisingly, Washington, D.C. (715) and Massachusetts (710) are states where Millennials’ average FICO scores rank second and third-highest in the U.S.

Millennials in West Virginia (11), South Carolina (11.4), and Arizona (11.5) have the lowest DSCRs. Moreover, South Carolina (656) and West Virginia (659) are states where Millennials’ average FICO scores rank third and sixth-lowest in the U.S.

Total U.S. Consumer Debt:

Total consumer debt in America is $4.4 trillion.

Total revolving debt in America is $1 trillion.

Total nonrevolving debt in America is $3.4 trillion.

Credit Card Interest Rates:

U.S. commercial banks charged an average credit card interest rate of 14.51% in November 2021.

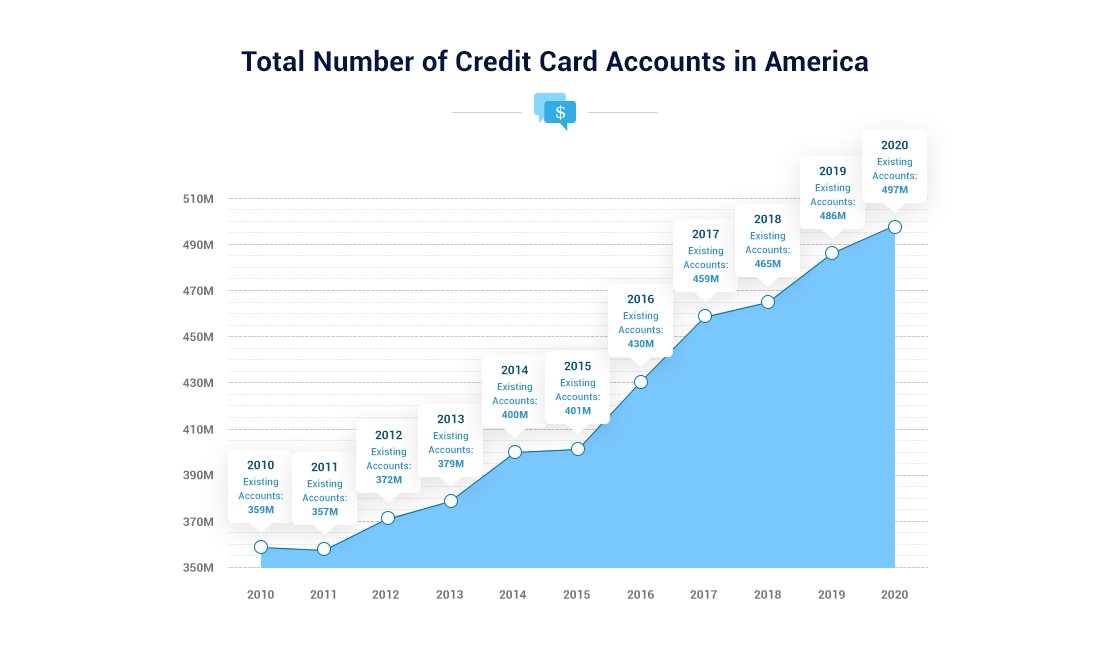

Americans hold 497M credit card accounts.

In 2020, Americans opened 12 million new credit card accounts. In 2019, this number was 21 million.

The average number of credit cards per American is 3.0 — the same as 2020 and 2019.

Credit Card Delinquency Rates:

The percentage of credit card accounts 30-59 DPD is 2.30% — a decrease of 4% YoY.

The percentage of credit card accounts 60-89 DPD is 1.00% — a decrease of 23% YoY.

The percentage of credit card accounts 90-180 DPD is 1.00% — a decrease of 34% YoY.

Delinquency rates on credit card loans issued by U.S. commercial banks hit an all-time low of 1.57% in the third quarter of 2021.

With the average U.S. FICO Score hitting an all-time high of 716, the combination of higher asset prices and lower debt levels helped support U.S. creditworthiness.

And with U.S. commercial bank deposits increasing from $13.3 trillion in January 2020 to $17.7 trillion in November 2021, the tsunami of cash allowed Americans to pay their bills without having to swipe their credit cards. For context, commercial bank deposits are checking and savings accounts that enable Americans to withdraw their money at any time.

To that point, data from Experian shows that Americans’ average credit card balance fell by 6% year-over-year (YoY) in 2021 — declining from $5,897 to $5,525.

Moreover, credit utilization also slipped, with Americans only tapping a quarter of their available revolving credit lines.

| Segment: | 2019: | 2020: | 2021: | Change: |

| Average Credit Card Balance | $6,494 | $5,897 | $5,525 | – 6% |

| Average Number of Credit Cards | 3 | 3 | 3 | 0% |

| Average Revolving Utilization Rate | 30% | 26% | 25% | – 4% |

For more information on why the average U.S. FICO Score hit an all-time high in 2021, please see our report on how American household finances were uplifted during the pandemic.

To approximate the total amount of credit card debt in the U.S., we analyzed the Federal Deposit Insurance Corporation’s (FDIC) data. Every three months, the FDIC releases its Quarterly Banking Profile — which summarizes the financial results of all of the FDIC-insured institutions.

The data includes a breakdown of the total credit card loans outstanding. In a nutshell: the data tells us how much credit card debt FDIC-insured institutions have lent out to Americans.

If you analyze the table below, you can see that credit card loans by FDIC-insured institutions rose sharply from $713 billion in the first quarter of 2010 to $942 billion in the fourth quarter of 2019 (a 32% increase).

However, after peaking in Q4 2019, credit card loans by FDIC-insured institutions dropped to a four-year low of $761 billion in the first quarter of 2021. Moreover, the metric also declined quarter-over-quarter (QoQ) in Q2 2020 and Q3 2020 — the initial periods following the onset of the pandemic.

As a result, the data from the FDIC supports the findings from Experian.

| Date: | Total U.S. Credit Card Loans (Billions): |

| 2010:Q1 | $713 |

| 2010:Q2 | $692 |

| 2010:Q3 | $684 |

| 2010:Q4 | $702 |

| 2011:Q1 | $663 |

| 2011:Q2 | $668 |

| 2011:Q3 | $666 |

| 2011:Q4 | $688 |

| 2012:Q1 | $650 |

| 2012:Q2 | $665 |

| 2012:Q3 | $668 |

| 2012:Q4 | $696 |

| 2013:Q1 | $660 |

| 2013:Q2 | $670 |

| 2013:Q3 | $677 |

| 2013:Q4 | $691 |

| 2014:Q1 | $658 |

| 2014:Q2 | $678 |

| 2014:Q3 | $683 |

| 2014:Q4 | $718 |

| 2015:Q1 | $680 |

| 2015:Q2 | $701 |

| 2015:Q3 | $715 |

| 2015:Q4 | $756 |

| 2016:Q1 | $724 |

| 2016:Q2 | $746 |

| 2016:Q3 | $762 |

| 2016:Q4 | $800 |

| 2017:Q1 | $756 |

| 2017:Q2 | $780 |

| 2017:Q3 | $795 |

| 2017:Q4 | $865 |

| 2018:Q1 | $820 |

| 2018:Q2 | $837 |

| 2018:Q3 | $856 |

| 2018:Q4 | $903 |

| 2019:Q1 | $860 |

| 2019:Q2 | $881 |

| 2019:Q3 | $893 |

| 2019:Q4 | $942 |

| 2020:Q1 | $873 |

| 2020:Q2 | $808 |

| 2020:Q3 | $796 |

| 2020:Q4 | $822 |

| 2021:Q1 | $761 |

| 2021:Q2 | $792 |

| 2021:Q3 | $806 |

When broken down by generation, Americans’ appetite for credit card debt showcases a similar trend. For example, Experian’s data shows that average credit card balances declined across all age groups in 2021 — except for Generation Z. For context, the cohort’s average credit card balance increased from $2,197 in 2020 to $2,312 in 2021 (a 5% increase).

Likewise, all age cohorts — except for Gen Z — also recorded a decline in their revolving utilization ratios. As a result, it’s another indication that the heavy expansion of U.S. federal debt allowed consumers to avoid bearing the burden themselves.

| Generation: | Average CC Balance: | # of Credit Cards: | Revolving Utilization Ratio: |

| Generation Z (18-23) | $2,312 | 1.7 | 31.1% |

| Millennials (24-39) | $4,569 | 2.7 | 30.2% |

| Generation X (40-55) | $7,236 | 3.3 | 29.7% |

| Baby Boomers (56-74) | $6,230 | 3.4 | 21.4% |

| Silent Generation (75+) | $3,821 | 2.7 | 12.6% |

Interestingly, the New York Fed’s latest Household Debt and Credit Report showed that credit card limits hit an all-time high in the third quarter of 2021. As a result, while consumers may be less willing to borrow, lenders have increased the amounts they’re ready to lend.

Conversely, the Fed’s report showed that credit card delinquency rates (90+ days past due) eclipse delinquency rates for mortgage, auto, and student loans. Moreover, credit card borrowers aged 18 to 39 (Gen Z and Millennials) have the highest delinquency rates across all generations.

To determine the average U.S. credit score by age, we analyzed the Fed’s latest Survey of Consumer Finances (SCF) report. For context, the report was compiled in 2019 and is the most recent survey available. However, Fed data shows a strong positive correlation between Americans’ median annual incomes and their average credit card debt.

For example, borrowers with median annual incomes of $16,290 or less have $3,830 in average credit card debt. Conversely, borrowers with median annual incomes of $290,160 or more have $12,600 in average credit card debt.

The findings make logical sense due to the relationship between assets and creditworthiness. To explain, high-income Americans often have stable jobs, own their homes, and maintain large investment portfolios. As a result, their potential collateral increases their creditworthiness in the eyes of lenders.

On the flip side, low-income Americans often live paycheck-to-paycheck and have little in the form of savings or investments. As such, this decreases their creditworthiness in the eyes of lenders.

| Income Percentile: | Median Annual Income: | % of Americans with Credit Card Debt: | Average Credit Card Debt: |

| < 20 | $16,290 | 30.5% | $3,830 |

| 20–39 | $35,630 | 45.6% | $4,650 |

| 40–59 | $59,050 | 55.0% | $4,910 |

| 60–79 | $95,700 | 56.8% | $6,990 |

| 80–89 | $151,700 | 45.9% | $9,780 |

| 90–100 | $290,160 | 32.2% | $12,600 |

As mentioned above, Americans’ income is highly correlated with their credit card debt. And with the U.S. Department of Labor (DOL) revealing that women earn roughly 82% of men’s median salary, their ability to access credit is somewhat diminished relative to their male counterparts.

In addition, the U.S. Fed found that women often have higher debt usage, longer credit histories, higher debt outstanding, increased use of credit revolvers, and higher installment loan balances than men. Moreover, delinquency rates are higher in women than men. However, males often exhibit higher rates of bankruptcy.

On top of that, 19% of men charge more than $2,000 per month to their credit cards. Conversely, only 8% of women admit to achieving this milestone.

All in all, American men carry average credit card debt of $7,407, while American women carry average credit card debt of $5,245.

ElitePersonalFinance analysis of FDIC data.

Across the racial spectrum, White Americans ($6,940) have the highest average credit card debt, while Black Americans ($3,940) have the lowest average credit card debt. Moreover, a survey by Credit Sesame found that 67% of White Americans have at least one credit card, while only 53% of Black Americans achieved this milestone.

And why is this the case?

Unfortunately, Black Americans have the lowest average credit score among all racial groups. And with low credit scores often restricting Black Americans’ access to credit, the dynamic traps them in a vicious circle.

For example, Americans’ income is highly correlated with their credit card debt and credit scores. And data from the U.S. Bureau of Labor Statistics (BLS) shows that median weekly earnings for White Americans 16 or over in the third quarter of 2021 were $1,024. Conversely, median weekly earnings for Black Americans 16 or over in the third quarter of 2021 were $799.

On top of that, the Consumer Financial Protection Bureau (CFPB) found that Black and Hispanic Americans are more likely to have errors and disputes on their credit profiles than other races. As a result, it’s often an uphill battle for Black Americans to increase their creditworthiness in the eyes of lenders.

| Race: | Average Credit Card Debt: |

| White | $6,940 |

| Black | $3,940 |

| Hispanic | $5,510 |

| Other | $6,320 |

| All Races | $6,270 |

ElitePersonalFinance analysis of FDIC data.

However, because of the COVID, all states decreased their average credit card debts.

Breaking down the data further, Experian found that Millennials — aged 25 to 40 — differed materially in their average incomes, credit card debt, and FICO Scores.

On one side of the coin, Millennials in Alaska ($5,388), Washington, D.C. ($5,118), and New Jersey ($5,034) have the highest average credit card debt. On the other side of the coin, Millennials in Mississippi ($3,724), Kentucky ($3,826), and Vermont ($3,843) have the lowest average credit card debt.

Also interesting, there is a strong correlation (0.74) between Millennials’ average credit card debt service coverage ratios (DSCRs) and their average FICO Scores. For context, we calculate the ratios by dividing Millennials’ average incomes by their average credit card debt.

And parsing the data, we found that Millennials in Massachusetts (18.7), Washington, D.C. (17.6), and Connecticut (16.5) have the highest DSCRs. And unsurprisingly, Washington, D.C. (715) and Massachusetts (710) are states where Millennials’ average FICO scores rank second and third-highest in the U.S.

Conversely, Millennials in West Virginia (11), South Carolina (11.4), and Arizona (11.5) have the lowest DSCRs. Moreover, South Carolina (656) and West Virginia (659) are states where Millennials’ average FICO scores rank third and sixth-lowest in the U.S.

| State: | Average Credit Card Debt: | Average # of Credit Cards: | Average Income: | Average FICO Score: |

| Alaska | $5,388 | 2.79 | $65,501 | 691 |

| Washington, D.C. | $5,118 | 3.07 | $90,043 | 715 |

| New Jersey | $5,034 | 3.85 | $77,193 | 702 |

| Virginia | $4,999 | 3.23 | $63,969 | 694 |

| Connecticut | $4,975 | 3.55 | $81,848 | 698 |

| Hawaii | $4,948 | 3.16 | $60,807 | 704 |

| Florida | $4,888 | 3.46 | $58,441 | 671 |

| Texas | $4,885 | 3.43 | $57,794 | 667 |

| Colorado | $4,841 | 3.23 | $66,679 | 702 |

| New York | $4,786 | 3.58 | $78,404 | 701 |

| Maryland | $4,777 | 3.25 | $70,002 | 690 |

| Nevada | $4,725 | 3.43 | $55,577 | 670 |

| North Dakota | $4,712 | 3.08 | $65,914 | 706 |

| Washington | $4,582 | 3.25 | $70,441 | 710 |

| Rhode Island | $4,581 | 3.56 | $61,624 | 694 |

| California | $4,578 | 3.61 | $74,304 | 697 |

| Georgia | $4,573 | 3.14 | $54,442 | 662 |

| Wyoming | $4,571 | 2.78 | $63,589 | 689 |

| Illinois | $4,568 | 3.54 | $67,243 | 692 |

| New Hampshire | $4,483 | 3.20 | $68,126 | 703 |

| Kansas | $4,450 | 3.15 | $58,380 | 690 |

| Delaware | $4,441 | 3.33 | $57,504 | 678 |

| Montana | $4,410 | 2.87 | $55,533 | 696 |

| Massachusetts | $4,396 | 3.31 | $81,995 | 710 |

| Arizona | $4,394 | 3.27 | $50,373 | 676 |

| Nebraska | $4,394 | 3.25 | $61,289 | 703 |

| Oklahoma | $4,355 | 2.90 | $51,564 | 660 |

| Pennsylvania | $4,353 | 3.40 | $63,276 | 693 |

| South Carolina | $4,352 | 2.92 | $49,737 | 656 |

| North Carolina | $4,302 | 3.11 | $52,568 | 676 |

| Tennessee | $4,254 | 2.96 | $53,340 | 670 |

| Minnesota | $4,243 | 3.14 | $64,674 | 716 |

| Utah | $4,236 | 3.15 | $53,539 | 707 |

| South Dakota | $4,232 | 2.77 | $62,446 | 704 |

| Louisiana | $4,230 | 2.90 | $53,281 | 658 |

| West Virginia | $4,213 | 3.08 | $46,343 | 659 |

| Missouri | $4,192 | 3.11 | $54,120 | 677 |

| Ohio | $4,154 | 3.29 | $55,767 | 682 |

| New Mexico | $4,152 | 2.99 | $48,161 | 664 |

| Oregon | $4,090 | 3.10 | $58,544 | 703 |

| Maine | $4,038 | 2.89 | $55,634 | 691 |

| Alabama | $4,017 | 2.79 | $48,133 | 653 |

| Idaho | $4,003 | 3.13 | $50,240 | 694 |

| Arkansas | $3,990 | 2.94 | $49,079 | 658 |

| Iowa | $4,303 | 3.05 | $56,457 | 697 |

| Michigan | $3,975 | 3.19 | $54,864 | 685 |

| Indiana | $3,959 | 3.09 | $54,625 | 678 |

| Wisconsin | $3,920 | 3.17 | $57,360 | 703 |

| Vermont | $3,843 | 2.79 | $60,396 | 706 |

| Kentucky | $3,826 | 2.99 | $49,259 | 667 |

| Mississippi | $3,724 | 2.70 | $44,128 | 644 |

With total U.S. consumer debt hitting another all-time high in November 2021, aggregate credit remains in an uptrend.

| Month: | Revolving Debt (Billions): | Nonrevolving Debt (Billions): | Total Outstanding Debt (Billions): |

| January 2021: | $961.53 | $3,221.73 | $4,183.26 |

| February 2021: | $965.00 | $3,238.51 | $4,203.51 |

| March 2021: | $966.40 | $3,256.49 | $4,222.89 |

| April 2021: | $965.29 | $3,274.16 | $4,239.45 |

| May 2021: | $974.44 | $3,298.17 | $4,272.61 |

| June 2021: | $992.11 | $3,315.03 | $4,307.14 |

| July 2021: | $997.93 | $3,324.79 | $4,322.72 |

| August 2021: | $1,001.11 | $3,335.06 | $4,336.17 |

| September 2021: | $1,010.87 | $3,353.13 | $4,364.00 |

| October 2021: | $1,017.45 | $3,363.44 | $4,380.89 |

| November 2021: | $1,037.41 | $3,377.33 | $4,414.74 |

Another reason for the increase might be that many lenders have changed their approval criteria, making their products more accessible for people. As a result, this increases consumers’ chances of approval and their potential loan balances. However, many lenders shut down their operations, while others raised their approval criteria.

For your reference, the chart below depicts how consumers’ total, revolving, and nonrevolving debt have evolved historically.

ElitePersonalFinance analysis of Federal Reserve data

Parsing through the Fed’s latest Consumer Credit report, we found that U.S. commercial banks charged an average credit card interest rate of 14.51% in November 2021. Moreover, while the U.S. Federal Funds Rate and U.S. Treasury yields have declined materially since 2019, U.S. commercial banks’ average credit card interest rate has only dropped slightly. To that point, with the metric increasing from 11.82% in August 2014 to 14.51% in November 2021, credit card borrowers haven’t benefited from the downtrend in U.S. interest rates.

| Date: | U.S. Commercial Banks’ Credit Card Interest Rate: |

| 2010-01-01 | 13.60% |

| 2010-02-01 | 14.26% |

| 2010-03-01 | 14.26% |

| 2010-04-01 | 14.26% |

| 2010-05-01 | 13.84% |

| 2010-06-01 | 13.84% |

| 2010-07-01 | 13.84% |

| 2010-08-01 | 13.59% |

| 2010-09-01 | 13.59% |

| 2010-10-01 | 13.59% |

| 2010-11-01 | 13.44% |

| 2010-12-01 | 13.44% |

| 2011-01-01 | 13.44% |

| 2011-02-01 | 13.44% |

| 2011-03-01 | 13.44% |

| 2011-04-01 | 13.44% |

| 2011-05-01 | 12.89% |

| 2011-06-01 | 12.89% |

| 2011-07-01 | 12.89% |

| 2011-08-01 | 12.28% |

| 2011-09-01 | 12.28% |

| 2011-10-01 | 12.28% |

| 2011-11-01 | 12.36% |

| 2011-12-01 | 12.36% |

| 2012-01-01 | 12.36% |

| 2012-02-01 | 12.34% |

| 2012-03-01 | 12.34% |

| 2012-04-01 | 12.34% |

| 2012-05-01 | 12.06% |

| 2012-06-01 | 12.06% |

| 2012-07-01 | 12.06% |

| 2012-08-01 | 11.95% |

| 2012-09-01 | 11.95% |

| 2012-10-01 | 11.95% |

| 2012-11-01 | 11.88% |

| 2012-12-01 | 11.88% |

| 2013-01-01 | 11.88% |

| 2013-02-01 | 11.94% |

| 2013-03-01 | 11.94% |

| 2013-04-01 | 11.94% |

| 2013-05-01 | 11.95% |

| 2013-06-01 | 11.95% |

| 2013-07-01 | 11.95% |

| 2013-08-01 | 11.88% |

| 2013-09-01 | 11.88% |

| 2013-10-01 | 11.88% |

| 2013-11-01 | 11.85% |

| 2013-12-01 | 11.85% |

| 2014-01-01 | 11.85% |

| 2014-02-01 | 11.83% |

| 2014-03-01 | 11.83% |

| 2014-04-01 | 11.83% |

| 2014-05-01 | 11.83% |

| 2014-06-01 | 11.83% |

| 2014-07-01 | 11.83% |

| 2014-08-01 | 11.82% |

| 2014-09-01 | 11.82% |

| 2014-10-01 | 11.82% |

| 2014-11-01 | 11.99% |

| 2014-12-01 | 11.99% |

| 2015-01-01 | 11.99% |

| 2015-02-01 | 11.98% |

| 2015-03-01 | 11.98% |

| 2015-04-01 | 11.98% |

| 2015-05-01 | 12.04% |

| 2015-06-01 | 12.04% |

| 2015-07-01 | 12.04% |

| 2015-08-01 | 12.10% |

| 2015-09-01 | 12.10% |

| 2015-10-01 | 12.10% |

| 2015-11-01 | 12.22% |

| 2015-12-01 | 12.22% |

| 2016-01-01 | 12.22% |

| 2016-02-01 | 12.31% |

| 2016-03-01 | 12.31% |

| 2016-04-01 | 12.31% |

| 2016-05-01 | 12.16% |

| 2016-06-01 | 12.16% |

| 2016-07-01 | 12.16% |

| 2016-08-01 | 12.51% |

| 2016-09-01 | 12.51% |

| 2016-10-01 | 12.51% |

| 2016-11-01 | 12.41% |

| 2016-12-01 | 12.41% |

| 2017-01-01 | 12.41% |

| 2017-02-01 | 12.54% |

| 2017-03-01 | 12.54% |

| 2017-04-01 | 12.54% |

| 2017-05-01 | 12.77% |

| 2017-06-01 | 12.77% |

| 2017-07-01 | 12.77% |

| 2017-08-01 | 13.08% |

| 2017-09-01 | 13.08% |

| 2017-10-01 | 13.08% |

| 2017-11-01 | 13.16% |

| 2017-12-01 | 13.16% |

| 2018-01-01 | 13.16% |

| 2018-02-01 | 13.63% |

| 2018-03-01 | 13.63% |

| 2018-04-01 | 13.63% |

| 2018-05-01 | 14.14% |

| 2018-06-01 | 14.14% |

| 2018-07-01 | 14.14% |

| 2018-08-01 | 14.38% |

| 2018-09-01 | 14.38% |

| 2018-10-01 | 14.38% |

| 2018-11-01 | 14.73% |

| 2018-12-01 | 14.73% |

| 2019-01-01 | 14.73% |

| 2019-02-01 | 15.09% |

| 2019-03-01 | 15.09% |

| 2019-04-01 | 15.09% |

| 2019-05-01 | 15.13% |

| 2019-06-01 | 15.13% |

| 2019-07-01 | 15.13% |

| 2019-08-01 | 15.10% |

| 2019-09-01 | 15.10% |

| 2019-10-01 | 15.10% |

| 2019-11-01 | 14.87% |

| 2019-12-01 | 14.87% |

| 2020-01-01 | 14.87% |

| 2020-02-01 | 15.09% |

| 2020-03-01 | 15.09% |

| 2020-04-01 | 15.09% |

| 2020-05-01 | 14.52% |

| 2020-06-01 | 14.52% |

| 2020-07-01 | 14.52% |

| 2020-08-01 | 14.58% |

| 2020-09-01 | 14.58% |

| 2020-10-01 | 14.58% |

| 2020-11-01 | 14.65% |

| 2020-12-01 | 14.65% |

| 2021-01-01 | 14.65% |

| 2021-02-01 | 14.75% |

| 2021-03-01 | 14.75% |

| 2021-04-01 | 14.75% |

| 2021-05-01 | 14.61% |

| 2021-06-01 | 14.61% |

| 2021-07-01 | 14.61% |

| 2021-08-01 | 14.54% |

| 2021-09-01 | 14.54% |

| 2021-10-01 | 14.54% |

| 2021-11-01 | 14.51% |

For more information, please see our study on Average Credit Card Interest Rates of July 2025.

| Year: | Existing Accounts: |

| 2010 | 359M |

| 2011 | 357M |

| 2012 | 372M |

| 2013 | 379M |

| 2014 | 400M |

| 2015 | 401M |

| 2016 | 430M |

| 2017 | 459M |

| 2018 | 465M |

| 2019 | 486M |

| 2020 | 497M |

In 2020, Americans opened 12 million new credit card accounts. In 2019, this number was 21 million.

We can’t say that 12 million is a low number, but this makes sense if we compare it to these 21 million in 2019.

Like we said above, COVID puts higher approval criteria on credit card issuers. The government makes people pay their debt and use their credit card limits less than before. The crisis makes people start saving more money instead of making unnecessary purchases.

And even if the average credit card interest rates now are lower, the number of newly opened credit card accounts significantly drop, compared to the previous period.

As a result, the average number of credit cards per person in America in 2021 slightly dropped. Not it is 3.0 before it was 3.07.

Read our complete study for those who want to learn more about the Average Number of Credit Cards Per Person of July 2025

There you will find all national average numbers and a detailed analysis showing these numbers by state, by age, by income, by race, by education, and much more interesting findings.

When borrowers fail to make the minimum monthly payments on their credit cards for 30+, 60+, or 90+ days, their loans are considered delinquent. And with Experian outlining in its latest State of Credit report that consumers’ delinquency rates declined again in 2021, it’s another sign that government stimulus helped consumers avoid a more ominous fate.

For context, the table below depicts the percentage of Americans with credit card accounts that are 30+, 60+, and 90+ days past due (DPD):

| Segment: | 2019: | 2020: | 2021: | Change: |

| % of Accounts 30-59 DPD | 3.80% | 2.40% | 2.30% | – 4% |

| % of Accounts 60-89 DPD | 1.90% | 1.30% | 1.00% | – 23% |

| % of Accounts 90-180 DPD | 6.60% | 3.80% | 2.50% | – 34% |

To that point, data from the Fed supports Experian’s findings. For example, delinquency rates on credit card loans issued by U.S. commercial banks hit an all-time low of 1.57% in the third quarter of 2021. Moreover, the metric has declined sharply from the 5.78% delinquency rate witnessed in the first quarter of 2010.

| Date: | U.S. Commercial Banks’ Credit Card Delinquency Rate: |

| 2010:Q1 | 5.78% |

| 2010:Q2 | 5.10% |

| 2010:Q3 | 4.58% |

| 2010:Q4 | 4.14% |

| 2011:Q1 | 3.82% |

| 2011:Q2 | 3.65% |

| 2011:Q3 | 3.45% |

| 2011:Q4 | 3.25% |

| 2012:Q1 | 3.06% |

| 2012:Q2 | 2.92% |

| 2012:Q3 | 2.82% |

| 2012:Q4 | 2.71% |

| 2013:Q1 | 2.64% |

| 2013:Q2 | 2.53% |

| 2013:Q3 | 2.44% |

| 2013:Q4 | 2.38% |

| 2014:Q1 | 2.32% |

| 2014:Q2 | 2.26% |

| 2014:Q3 | 2.20% |

| 2014:Q4 | 2.15% |

| 2015:Q1 | 2.11% |

| 2015:Q2 | 2.12% |

| 2015:Q3 | 2.15% |

| 2015:Q4 | 2.16% |

| 2016:Q1 | 2.14% |

| 2016:Q2 | 2.21% |

| 2016:Q3 | 2.30% |

| 2016:Q4 | 2.37% |

| 2017:Q1 | 2.39% |

| 2017:Q2 | 2.48% |

| 2017:Q3 | 2.55% |

| 2017:Q4 | 2.49% |

| 2018:Q1 | 2.48% |

| 2018:Q2 | 2.49% |

| 2018:Q3 | 2.53% |

| 2018:Q4 | 2.55% |

| 2019:Q1 | 2.51% |

| 2019:Q2 | 2.58% |

| 2019:Q3 | 2.63% |

| 2019:Q4 | 2.62% |

| 2020:Q1 | 2.66% |

| 2020:Q2 | 2.43% |

| 2020:Q3 | 2.02% |

| 2020:Q4 | 2.11% |

| 2021:Q1 | 1.85% |

| 2021:Q2 | 1.58% |

| 2021:Q3 | 1.57% |

ElitePersonalFinance always has up-to-date studies.

Our goal is to consolidate the information and present the findings in a way that’s easy to understand by parsing through the latest data from FICO, Equifax, Experian, and TransUnion. If you enjoyed the study, please provide your feedback. Moreover, if there is anything that we missed or anything that you believe needs updating, please let us know, and we will respond promptly.

With the U.S. federal debt making new all-time highs in 2020 and 2021, lawmakers unprecedented response to the COVID-19 pandemic helped ease the burden on consumers. And with the credit baton passed from individuals to the U.S. government, the latter’s spending spree provided some Americans with more cash than they needed.

As a result, consumers’ debt impulse declined, as robust balances in their checking and savings accounts eliminated the need for credit card debt. However, with inflation on the rise and lawmakers paring back their stimulus efforts, U.S. credit card debt will likely increase of July 2025.

| Age: | 2018: | 2019: | Change: |

| 20 – 29 | $2,581 | $2,709 | + 5% |

| 30 – 39 | $5,466 | $5,563 | + 1.8% |

| 40 – 49 | $7,750 | $7,922 | + 2.2% |

| 50 – 59 | $8,116 | $8,364 | + 3% |

| 60 – 69 | $6,701 | $6,832 | + 1.9% |

| 70 – 79 | $5,139 | $5,250 | + 2.1% |

| 80 – 89 | $2,876 | $2,990 | + 4% |

| 90 – 99 | $1,370 | $1,433 | + 4.6% |

As the statistics show that people between 50 – 59 have the greatest borrowing capacity. With an average credit card debt of $8,364, individuals between 50 – 59 use credit cards more often than their peers.

Consumers ages 40 to 69 have above-average credit card debt. According to Experian data, the average credit card debt for borrowers 40 to 69 was consistently above the national average of $6,194.

Millennials (< 30) and elderly (> 70), not so much.

Due to lower wages and the increasing costs of both housing and long-term care, these groups rely less on credit card debt to finance their lifestyle.