Credit reporting scoring models, updates to the Fair Credit Reporting Act (FCRA), changes to FICO algorithms, and ongoing changes to regulations around what’s reported to Experian, Equifax, and TransUnion have been revamped throughout 2025.

This comprehensive guide will walk you through everything you need to know to increase your credit score in 2025. In it, we’ll discuss everything from the latest credit scoring news shaping up 2025, how credit scores are calculated to responsible money management habits, strategic use of our favorite credit-building tools, how artificial intelligence is changing the game, how to achieve an 800 credit score, and virtually everything you need to know about credit reporting.

Thanks for trusting ElitePersonalFinance to provide the tools you need to revamp your credit score fast and quickly and take advantage of lower APRs and flexible repayment terms for sound peace of mind when taking on your next loan.

Expected Changes in 2025

Expect many changes to credit reporting and scoring models throughout 2025, including updates to Fair Credit Reporting Act guidelines, changes to how FICO calculates your credit score, and even how Buy Now Pay Later (BNPL) services like Klarna and Affirm report to bureaus.

Let’s grab a look at what to expect for the remainder of 2025:

Hello to FICO 10T Model

One of the most significant news items to hit FICO in 2025 is the updates to its credit scoring. Dubbed FICO 10T, which stands for trended data, it is a new scoring model based on predictive credit consumer risk management, expected to play an even more significant role with consumer credit this year.

Under 10T, lenders will now weigh heavier your past 24 months of credit activity, factoring in your number of late payments, increasing debt load, and the amount of spending you’ve done. For example, previous FICO scoring models may have prioritized late payments over the last two years a bit less versus now.

For example, you might have a spotless credit record for the last seven years. However, if you’ve maxed out your credit card limit utilization well past 80% or made two late payments within the past six months, the FICO 10T model will weigh it heavier against your credit score, affecting your ability to secure lower APR loans with the terms you’re looking for.

In short, your credit record for the last two years is now more representative of responsible borrowing behavior (and thus weighted heavier) than your spotless credit record for the preceding six or seven years.

Buy Now, Pay Later (BNPL) Reporting to Credit Bureaus

Now, BNPL services like Affirm will report your payment history to all three major credit bureaus, including TransUnion, Equifax, and Experian. For example, if you use Klarna to purchase a $580 WiFi mesh system from Amazon and go on to hit a 60-day late, expect it to appear on your credit report. A single missed payment or two consecutive missed payments could drop your score by 100 points or more.

Remember, these types of services allow you to pay off your balance in four equal installments (part of the Pay in 4 plan we’ve covered in previous ElitePersonalFinance guides), incentivizing borrowers to make larger purchases d and increase the likelihood of falling into a debt cycle.

Utility and Rent Payments Incoming

With the advent of utility and rent payment reporting programs like Experian Boost, these monthly payments now have more sway in your overall credit score calculation.

If you haven’t signed up for it, do so and take advantage of your rent and utility bills being paid on time for the last several years. Other services tallied include phone bills and streaming services like Netflix, which you can use to bump your credit score without taking out credit cards and installment loans.

To use Experian Boost, simply link your checking or savings account, select payments to include, and enjoy score tracking over time (assuming you have a history of on-time payments). Note, that these payments are only reported to Experian and not Equifax and TransUnion. Most lenders report to at least one if not two or all three of them, depending on the type (e.g. mortgages to all three credit bureaus).

Even More Artificial Intelligence

According to the AI in Fintech Global Market Report 2024 by Research and Markets, artificial intelligence within financial tech is expected to see massive market growth to the tune of $39.44 billion by 2028, driven by the need for banks, credit unions, and other financial institutions to improve their fraud detection, risk management, and even regulatory compliance through automation.

Another area that artificial intelligence focuses on is producing alternative credit scoring models, where AI-powered financial tech solutions have focused on other eligibility criteria to determine creditworthiness, such as your income patterns and spending behavior.

Credit Utilization Spikes

Another area of credit scoring focus in 2025 is stricter credit utilization impact, where spikes on credit card balances will be more heavily weighted. If you exceed 50% of your available credit at any point, then you’re more likely to take a hit on your credit score. Plus, there are alternative scoring models that are now placing a heavy emphasis on utilization trends over time, which may be more reflective of financial health.

Ongoing Employment and Income Verification

In 2025, you should also see a heavier emphasis placed on employment and income verification.

In the past, traditional credit score models have relied on the old FICO criteria, such as payment history and credit utilization ratio. However, artificial intelligence is putting a dent in it through real-time payroll data provided by services like Plaid, which allow creditors to evaluate a person’s creditworthiness based on earnings over time.

Without question, lender Upstart exemplifies this, applying a mix of artificial intelligence and machine learning to dip into alternative data points, including employment history, income, education, degree, and hundreds of other factors to provide an opportunity for applicants who might have had difficulty lending from traditional banks and credit unions. Expect Upstart to continue strong in 2025 and beyond.

Promising Credit Scoring Apps in Focus

Today there’s no shortage of apps and “AI engines” that make it easy for people to achieve their credit score goals.

For example, Dovly.ai promises the use of AI to help improve and repair your credit through personalized action plans and “AI-powered” dispute reporting with Experian, TransUnion, and Equifax for $39.99 a month through its Premium package.

Kudos for its free version which makes it accessible to everyone.

Other services that are similar to Dovly include Credit Karma, Experian Boost, Upstart, and TomoCredit. The common denominator with all of these is that they use artificial intelligence to analyze credit history, apply predictive analytics based on your spending habits, and evaluate non-traditional credit factors to do things like recommend repayment strategies and present customized credit card and loan offers for your financial situation.

In short, artificial intelligence promises to pay immediate dividends when it comes to automated dispute handling, personalized credit strategies, and speeding up approvals across all types of credit lines, no matter what your credit score is.

A Word on Medical Debt

According to the Consumer Financial Protection Bureau (CFPB), billions of dollars worth of medical bills will now be excluded from credit reports, which wipes an estimated $49 billion off the books, affecting roughly 15 million Americans.

Primarily, this will apply to medical bills under $500, which means a lot of doctor’s office visits will be naturally covered.

One of the biggest reasons for this overhaul is the fact that many feel medical debt unnecessarily penalizes people’s credit scores. Plus, they have a higher rate of going into collections, which could affect borrowers’ ability to apply for auto loans, mortgages, and other lines of credit at lower interest rates.

Introduction to Credit Scoring

Your financial reputation rests on credit scoring.

The higher your credit score, the greater your ability to acquire loans at favorable APR interest rates and repayment terms with greater transparency. As of 2025, two of the most widely used credit scoring models are FICO and VantageScore.

Of these, FICO is the most widely used credit scoring model. It bases your score on five weighted key criteria: payment history (35%), credit utilization (30%), length of credit history (15%), credit mix (10%), and new credit inquiries (10%). Based on these percentages, scores are assigned from 300 to 850.

Payment History (35%)

This is one of the most important factors to boost your credit score fast. Accounting for more than a third of your credit score, payment history reflects all your on-time monthly payments across your lines of credit, including credit cards, mortgages, and loans. Even a late payment can drop your score by 100 points or more. Generally, the more recent your late payment, the more significant the damage.

For example, if you miss a mortgage payment by 30 days, expect a 50-to 100-point drop, depending on your overall score. If it’s your first late payment in seven years, expect the minimum drop versus a steeper drop if you have fewer accounts in good standing or are in the process of rebuilding credit.

Pro Tip: One of the best ways to keep payment history 100% is to set up automatic minimum payments across all your credit accounts. Always establish an automatic backup for minimum payments and try to pay off the entire outstanding statement balance every month.

One of our favorite services for this is Monarch Money, an adequate Mint.com replacement.

Credit Utilization (30%)

Utilization refers to a ratio of your total outstanding balances on cards versus your available credit limit. The higher the percentage, the lower your score. Expect a 50 to 100-point drop if you max out one or more of your credit cards or if your credit utilization consistently hovers above 30%.

If you maintain your credit card balances below 10% utilization for a while, you can expect the most significant boost in your credit score.

Pro Tip: To reduce your amounts owed, try to pay off your balance before your statement’s closing date. Remember, lenders do not report balances on the due date but on the statement closing date. Paying off your outstanding balance before the closing date will keep your utilization ratio low (depending on your entire outstanding balance owed at the time).

Length of Credit History (15%)

Length of credit history refers to the average age of all of your accounts, starting from the age of your oldest account to the age of your newest account. It also factors in recently opened accounts. Generally, we recommend never closing any old credit card, even if there are $0 balances for years. Closing any of your top three of these accounts could cause a 10 to 50-point drop now that you have shortened the average age across all of your accounts.

Pro Tip: One of the best things you could do to keep your length of credit history intact is to set up small recurring charges as long as a dollar on an old card. Always try to keep your old cards active and never close them, even if you’re tempted to. Remember, every card has a credit history, and every credit history increases your average total account age.

Credit Mix (10%)

Credit refers to the different types of credit you manage daily and monthly, such as mortgages, auto loans, and credit cards. By working various kinds of credit and paying them on time, you’ve proven to lenders you can manage credit responsibly.

If you do not have a mortgage or auto loan and only rely on credit cards, we recommend adding a small personal loan or credit builder loan from a reputable credit union. Keep it small, so you don’t take on any additional debt.

Amount of New Credit Inquiries (10%)

The number of new credit inquiries refers to the increase in your credit report within a 14-day window while doing rate shopping. Always try to avoid multiple hard inquiries and pre-qualify whenever possible. Note that various hard inquiries for one type of loan, e.g., auto or home mortgage, typically classify as one inquiry, so you don’t have to worry about temporary scoring dips.

General Stats on Credit Scores

The Consumer Financial Protection Bureau has a treasure trove of insights that provide insight into how Americans are using their general purpose credit cards. To start with general stats, as of June 2024, around 6.7 million credit cards were distributed with a total credit limit of 4$1.4 billion dollars.

At the same time, there was also a 7.6% increase in originations with a higher 17.7% increase in year-over-year inquiries.

For more information on origination activity, visit CFPB – Origination Activity, where you can see a series of graphs that give additional insights into lending levels, credit tightness (number of consumers applying for credit cards who do not apply for new credit), year-over-year changes, and even geographic changes such as percentage change in volume of new credit cards originated in each state.

For example, you’ll be surprised to know that there was a 24% increase in origination in North Dakota (2024) versus a negative 21% origination rate in Iowa.

All in all, the CFPB offers insightful analysis into the state of credit cards in the United States today, all good background information to have before learning how to increase your credit score in 2025.

Noticeable vs. Non-Obvious: How to Increase Your Credit Score

Obvious: Pay Bills On Time

With payment history accounting for 40% of your credit score, staying on top of this includes setting up auto-pay (for at least the minimum amounts on every statement balance) and paying off any debt ASAP. Remember, your credit score will take a hit when it’s at least 30 days overdue, with nothing reported before that.

If you exceed the 30-day mark, call your creditor and request a goodwill adjustment. Those with a good, excellent payment history can often have late marks removed with a little bit of phone or email negotiation.

Not So Obvious: Request Credit Limit Increase

Another excellent trick to lower your credit utilization ratio is to request a credit limit increase.

Credit card issuers can adjust your limits every 6 to 12 months without requiring a hard inquiry. For example, if you have a $10,000 limit, a $4,000 balance, and a 40% utilization ratio, raising your limit to $20,000 will drop your utilization ratio to 20%. As long as overall spending remains the same, you should see an extra 20% to 50% boost to your credit score within a few months.

Obvious: Keep Your Credit Utilization Below 10%

If you want to enjoy a 30- to 80-point boost within a few months, keep your credit utilization ratio low by 10%. Ways to maximize this include paying off your credit card several times a month (versus the statement due date), calling your bank for the dates they report balances to credit bureaus, spreading high balances across multiple cards, and keeping your utilization ratio at or under 10%.

Generally, those who enjoy 800-plus credit scores almost always have utilization in the 5% range. That’s why it’s always up to them to achieve the score.

Not-So-Obvious: Become an Authorized User

For a 40 to 100-point boost within months, another not-so-obvious increase in your credit score is becoming an authorized user on someone with an excellent credit history. This allows you to take advantage of the average account age and history of on-time payments.

Preferably, this person has a minimum of 10 years of on-time payments. Try to go with a trusted family member or friend with excellent credit in 800+ territory.

Not-So-Obvious: Pay Your Credit Card Bill Twice a Month Instead of Once

You can boost your credit card by paying your bill twice a month as it is supposed to. Adding an extra mid-month payment keeps your reported balance as low as possible, bumping your score by as much as 40 points over several months.

Not-So-Obvious: Take Out Credit Builder Loans

Did you know you can take out credit builder loans even if you have good credit? Unlike traditional loans, fixed monthly payments are made while qualified lenders use a security account to hold borrowed funds. After you finish paying it off, you get the funds back, and all of your on-time payments get passed on to Experian, Equifax, and TransUnion.

One of the best things about this is that you don’t need to take out a credit card to start building your payment history. It’s a great way for those with limited to no credit, such as college students, to start building credit and for experienced borrowers to diversify their credit mix even further. Remember, credit mix accounts for 10% of your credit score.

Expect a boost of your credit score up to 70 points if you take out even a small $500 credit builder loan and pay it back within 12 months. Just be sure you do not miss a single payment!

Not-So-Obvious: Dispute Errors on Your Credit Report

One of the quickest ways to boost your credit score is by successfully disputing an error on your Experian, Equifax, or TransUnion credit reports. Any errors can appear due to miscalculations, such as accounts not belonging to you listed, incorrect payments, outstanding debts already paid off, etc.

For example, suppose you find an erroneous $5,000 collection account on a non-existent medical bill. In that case, you can dispute it with all three major reporting credit bureaus with supporting documentation, and your score should jump.

You can download a free credit report from annualcreditreport.com, review the details with a fine-tooth comb, and file a dispute online using each bureau’s contact information.

By law, every credit bureau has up to 30 days to respond, and the most successful disputes can be resolved in as little as 45 days. When taking out large loans like auto and home mortgages, we recommend doing this to see a greater likelihood of enjoying lower APRs and better terms.

Word on Drops

Have you ever experienced a sudden drop in your credit score and wondered what caused a 10-point, 50-point, 100-point, or 200-point decrease?

Let’s explore several scenarios that can cause these drops in your score:

10 Points

Small dips of 10 points on your credit score are usually the result of small things such as a slight raise in your credit utilization ratio or a single hard inquiry. Hard inquiries can typically dip your score anywhere from 5 to 10 points. The same goes for your utilization. If it goes up by single-digit percentage points, you can expect a small decrease, but it’s very easy to get it back up as long as you pay off the outstanding balance quickly.

50 Points

A 50-point drop in credit score is usually caused by a single late payment or bumped credit utilization from 30% to 40%. For example, if you have a 720 FICO score with a recent 30-day late payment and it’s your first payment in a very long time with a relatively strong profile, then you could see this type of dip.

Another example is if you max out a credit card with utilization on that card shooting about 80%. In that case, your score can drop from 730 to 680 even if you make monthly on-time payments. Always try to keep your utilization ratio under 30% (and preferably at 10% or under), where you can see your score increase back within a matter of weeks.

100 Points

Suppose your score drops by 100 points. In that case, it’ll address egregious issues with your credit reporting, such as two consecutive late payments or one of your auto loans escalating to collections agencies.

Of course, the severity of dropping the score depends on several factors, such as the number of missed payments, your previous credit record, and the number of times debt has been previously sent to collections. Remember that debt is usually sent to collections after 60 days of delinquency, though not all creditors report late payments to credit bureaus.

200 Points or More

200-point drops to your credit score are usually caused by catastrophic circumstances such as bankruptcy and foreclosure.

For example, if you have a 680 credit score with more than one delinquency on one or more credit cards and a second account escalated to collections, your score can drop by as much as 200 points, potentially from 680 to 480. Regrettably, bankruptcy has a 10-year look-back window on your credit report, although it’s not impossible to resuscitate your score, albeit with a very long road ahead.

Regardless of whether these events drop your score by 50, 100, or 200 points, never face them in the first place! It’s not that difficult.

Who Reports Payments to Credit Bureaus?

One important thing to note with credit bureaus is that not all creditors report on-time or missed payments. Remember, the three major reporting bureaus are Equifax, Experian, and TransUnion, and any number of services can report payment history, including credit card issuers, mortgage lenders, personal loan providers, and student loan providers.

Here’s some topline information on who and who does not report payments to credit bureaus:

Credit Card Issuers: Expect all major banks, such as Bank of America and Wells Fargo, to report to all three bureaus. They provide a complete history, including your credit limit, spending balances, and utilization ratio.

Note, store-brand credit cards from TJ Maxx, Burlington, and others do report, but usually to one or two bureaus at best, not all three. These work like a secured credit card, which traditionally reports to all three bureaus.

Mortgage Lenders: All mortgage lenders report your payment history to Equifax and Experian, and sometimes to TransUnion. Even a single late mortgage payment can cause a 100-point drop in your score, compared to 200 points or more for foreclosures.

Auto Lenders: Most of the lenders report to Experian, Equifax, and TransUnion. This includes any number of banks and dealership-backed loans, with any 30-day late causing up to an 80-point drop versus repossession of an actual vehicle causing up to a 200-point drop. That’s why we encourage you to never apply for title loans.

Personal Loans: Not all private lenders report to all three bureaus, but you should expect them to report to at least one. Note, that federal student loans report payments through all three bureaus, with any going into default (usually a default of nine months or more) resulting in credit score drops of up to 150 points.

Buy Now, Pay Later (BNPL) Services: BNPL services like Klarna and Afterpay generally report late payments to at least one credit bureau (Experian). Note that missed BNPL services typically have lower score drops than personal and student loan providers, anywhere from 30 to 50 points (30 days late).

Rent & Utility Companies: Generally, your rent is not included in credit bureau reporting unless you use specialized services like Experian RentBureau to report voluntarily. Likewise for utility and phone providers, although late payments and defaults could be escalated to collections or debt agencies, resulting in a score drop of up to 100 points (depending on your existing credit history).

Two essential things to note are that any debt that goes into collections will be reported to all three bureaus, where even a single collections activity lowers your score by as much as 150 points, depending on your overall credit record. Our top recommendation is always to assume that creditors report payments before taking out any loan, knowing that a single late payment can remain on your record for up to seven years.

In short, credit card issuers, mortgage lenders, auto lenders, personal lenders, BNPL services, and rent & utility companies all have a part in reporting or not reporting your payment history to Experian, Equifax, and TransUnion.

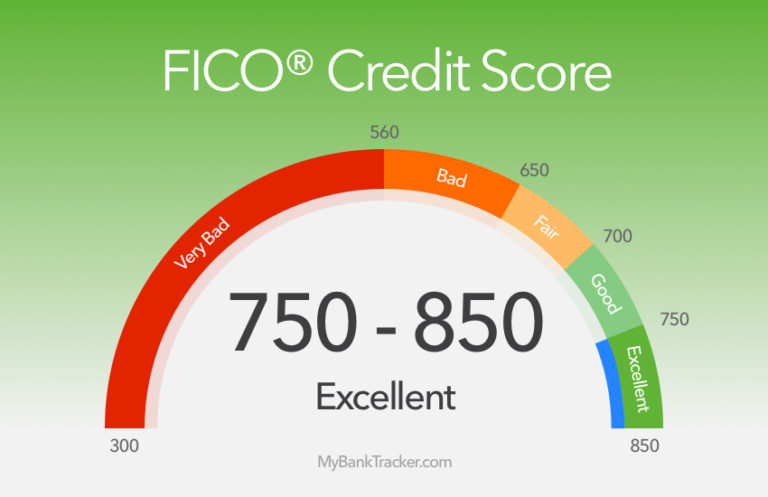

Understanding FICO’s Credit Score Tiers

Established by the Fair Isaac Corporation, FICO is the most popular credit scoring system. Thousands of lenders use it to evaluate an individual’s creditworthiness. Here are various categories and their respective score ranges.

Poor: 300–579

Classified as the lowest level, falling into this category guarantees you will have difficulty taking out most credit or loan opportunities now that you are a high-risk borrower. Expect apps, credit cards, and personal loans for bad credit to range anywhere from 31.99% to 35.99%, which helps upset the risk of lenders assuming lending to those with limited to no credit history.

Fair: 580–669

Consumers who fall into this range typically have several missed payments or high balances with utilization ratios above 40% on their records. Expect more credit opportunities than those with poor credit scores and higher-than-average interest rates and fees. Expect APIs, credit cards, and personal loans to fall between 24% to 31.99%.

Good: 670–739

Consider yourself having a solid but not excellent credit history, with competitive interest rates ripe for the taking. APRs, credit cards, and personal loans in the 12% to 20% territory is fair game.

Very Good: 740–799

Consumers falling into this category have an excessive track record of making on-time payments, solid debt management, and enjoying lower-than-average interest rates on loans and credit cards. APRs on credit cards and personal loans can fall as low as 9% to 16%.

Excellent: 800–850

Reserved for a select few, having an excellent credit score allows you to take advantage of the very best interest rates and repayment terms. Expect credit card and personal loan rates to fall from 6% to 12%. Plus, you can take advantage of premium-level credit cards like Chase Sapphire and American Express that come with premium rewards, warranty coverage, roadside assistance, concierge services, and a lot more.

Let’s Discuss APRs

Note that APRs across all of these scoring categories come with caveats. For example, credit unions cap APRs at 18%, typically qualifying people in the Good to Very Good scoring range. Another thing to consider is understanding the different types of APR credit cards based on the kind of balance and your overall credit profile.

As for purchases, APR is a standard interest rate applied to all purchases but typically ranges anywhere from 6% to 30%. In turn, cash advance APRs charge higher APRs, and regular purchases add up to 30%, with interest occurring from the first day immediately after withdrawing cash through an ATM or bank.

Lastly, consider balance transfer APRs (rates from 0% to 25% when moving from one card to another, with occasional 0% introductory APRs), penalty APRs for missing payments, or APRs for a certain number of months on purchasing balance transfers on balance transfer cards, with regular purchase APRs following immediately after the end of the promotional period.

Understanding FICO’s credit scoring tiers and different types of APRs can influence anyone’s ability to get a good credit opportunity. By understanding both of these terms, you’ll be in a better position to be on solid financial footing as you work to improve your credit score and navigate through all the different types of loans out there.

A Word on Alternative Credit Scoring Models

Although FICO and VantageScore are the most widely used scoring models, plenty of alternative credit scoring models are entering the mix.

Here are some of the more popular ones:

Experian Boost

Experian Boost, which promises to “instantly raise your credit scores for free” on its web page, allows anyone to contribute a favorable rent and utility bill history to their credit scores. Historically, on-time payments have not been recognized by any credit bureaus, with a lean towards credit cards and installment loans instead. These non-traditional payments are included, allowing those with limited to no credit history to be put on a more level playing field.

To qualify, you need only connect your bank accounts, select the bills you want to use (e.g., Verizon and Hulu), and see your results on the Experian Boost website within days.

In addition to the services, you can also ask if you can get a free credit score, get a credit card and loan offers, and even run a free identity scan that allows you to see if your information is available on the Dark Web, lowering your chances of identity theft.

TransUnion CreditVision

TransUnion’s equivalent to Experian Boost, CreditVision, takes into consideration other criteria outside of a history of late payments and utilization. It focuses mainly on trends like how low your debt is decreasing over time or how much you’re saving over time. It’s an excellent alternative scoring model for people trying to do their best rather than be tied to past credit behaviors.

FICO Score XD

Suppose you have limited to no credit history. In that case, FICO Score XD can step up to the plate by allowing you to introduce other creditors to your overall score, such as utility and public records, allowing you to lower APRs on loans and credit cards. For example, many people may be behind on auto loans, mortgages, and credit cards. Still, not so much on phone bill payments and other recurring subscriptions, so FICO Score XD provides a more even picture of creditworthiness, especially for younger folks.

Equifax Ignite

Equifax Ignite is a bit more advanced than Experian and TransUnion in that it uses artificial intelligence and machine learning to scour your banking transactions and social media activity to determine your creditworthiness. It’s not used that much by financial institutions but can be used to evaluate risk outside of traditional scoring models.

Upstart

Unlike Experian Boost, TransUnion CreditVision, and Equifax Ignite, Upstart is an actual AI lending platform that forgoes FICO scores and bases a person’s loan eligibility on factors like education, employment record, income, and incoming cash flow. If you have an extensive credit history but substantial income, it could be especially beneficial.

According to Upstart, its platform approves 27% more borrowers than traditional lending models. It also offers 43% lower rates than the same model, making it an excellent alternative for people with poor, fair, or bad credit.

All in all, alternative scoring models have hit the scene in recent years thanks to the infusion of traditional credit scoring models and more real-world scenarios, such as incoming cash flow, education, employment history, and other factors that assess a person’s creditworthiness just as well.

What’s The Difference Between FICO and VantageScore?

Two of the more popular credit scoring models, FICO and VantageScore, differ very slightly in how they interpret minimum credit history requirements, late payment methods, the impact of credit inquiries, and other factors that go into calculating your credit score.

For example, scoring regions are similar, with FICO going from 300 to 850 (versus the same for VantageScore). However, FICO requires at least six months of credit history, whereas VantageScore requires one month. In addition, late payments are weighted equally on VantageScore versus disproportionately with FICO, which leans towards late mortgage payments impacting scores more so.

Even trended data is treated differently between FICO and VantageScore, where FICO primarily looks at static data versus trended data for the other (meaning there’s an increased emphasis on how consumer credit behavior has evolved).

Regarding overall adoption, FICO is used by 90% of top lenders across all types of credit offerings, including mortgage and auto loans. In turn, VantageScore is more popular with credit card issuers and landlords.

5 Credit Score Myths Debunked

Within the world of credit scoring, there are a lot of myths that people abide by.

However, it’s time to dispel five of our pet peeves:

Checking Your Credit Score Lowers It

Under no circumstances will Experian, Equifax, or TransUnion lower your credit score if you keep checking your credit reports. Remember that there are two types of inquiries: soft and hard, with soft inquiries occurring when you check your credit versus lender pre-qualification. Do not hesitate to continue checking your credit score using Experian Boost, Credit Karma, or even through your bank if they offer such a program (e.g., Chase Banking).

In turn, hard inquiries do cause a temporary dip in your score by as little as five points whenever your lenders pull your credit to examine your eligibility.

Carrying a Small Credit Card Balance Worsens Your Score

Do not follow any assumptions that carrying a balance helps your credit. Remember that interest charges accumulate if you have an outstanding balance, and the utilization ratio is a factor. Try to keep it to no more than 30% of your available credit. Always ensure you pay off your credit card in full every month or at least keep your balance below 10% of your credit limit.

Closing Old Accounts Helps Your Score

Under no circumstances does closing old accounts help your credit score. Remember that the length of your credit history is 15% of your FICO score, so any closed account will immediately shorten your average credit age. Plus, you might even leverage an old account to lower your overall utilization ratio, which contributes to an even higher percentage of your score.

In short, old accounts are more valuable than you think! Kudos to any of them that do not carry any annual fees, so they do not create an extra financial burden for you.

You Only Need One Credit Card to Start Your Credit History

Although credit comprises only 10% of your FICO score, it’s always better to have a mix of different types of credit, including auto loans, mortgages, credit cards, and other types of installment loans. One of the best ways to boost it in no time is to take out a small personal loan and make on-time payments.

For example, if you only have credit cards, take out an installment loan and always avoid opening too many accounts at once.

High Income = Higher Credit Score

Credit scores have nothing to do with how much you make. You can earn $500,000 a year and have a credit utilization ratio of 70%, which takes 100 points or more off of your score. Despite high income, it’s not uncommon for fair credit borrowers to have credit scores in the 620 range, whereas low earners with utilization below 10% hover in the $780+ territory.

Remember always to make on-time payments and keep your utilization ratio low, no matter your salary.

All in all, checking your credit score, closing old credit accounts, carrying a small credit card balance, only using one credit card, and having a high income do not matter when it comes to credit scoring. By debunking these myths, you’ll be well on your way to boosting your credit score in 2025.

Frequently Asked Questions

How can Buy Now, Pay Later (BNPL) services affect my credit score in 2025?

Unlike in recent years, BNPL services will weigh heavier on your credit score. Even a single payment can cut your score by up to 100 points, so we highly encourage you to make on-time payments every time.

How does medical debt removal from credit reports affect my score?

As mentioned in the above guide, the Consumer Financial Protection Bureau (CFPB) has now removed all medical debt from your credit report, so your score will be positively affected if medical bills have previously wreaked havoc on your record.

How do I increase my credit score if I have no credit history?

One of the best ways to increase your credit score if you have no credit history is by taking out a secured credit card or becoming an authorized user of someone else’s credit card. Taking advantage of someone else’s positive credit history can help boost your score if you manage your payments responsibly.

Can my employment history impact my credit score?

Yes, employment can impact your credit score. It all depends on the type of lender you’re working with. There are also online marketplaces like Upstart, which use artificial intelligence algorithms to determine credit rather than traditional credit scoring models.

Is it a good idea to open multiple credit cards to improve my credit score?

We recommend not opening multiple credit cards within a short time frame, as it will generate a lot of hard inquiries that can cause a temporary dip in your score. Plus, over time, it could increase your credit utilization ratio if you’re blowing past 40% utilization ratios on each or as the average.

How do I increase my credit score in 30 days?

There are several ways to increase your credit score in 30 days. Two recommended methods involve paying down revolving account balances and disputing inaccurate information on your credit report, which can boost your score by up to 100 points within a short time frame.

Is 650 a good credit score?

Within the FICO Zone scoring system, 650 is considered Fair, which doesn’t qualify you for the best APRs. At a very minimum, you should aim for 700 and up, which is considered good. Note that even with a 650 credit score, you can still find favorable credit cards with decent (not great) APRs and perks.

Can I remove a late payment from my credit report?

Yes, it is possible to remove late payments from your credit report, provided the entry is incorrect. You can dispute it with one of the three credit bureaus or via a goodwill letter that you write to the creditor, asking them to remove it from your record. If you have a strong history of on-time payments, then this is more likely to happen.

Otherwise, expect the late mark to stay on your credit report for up to seven years.

How does co-signing a loan affect my credit?

When cosigners sign off on a loan, it means they agree to become responsible for the debt. If the primary borrower defaults or produces late payments, that can influence your own credit and add to your utilization ratio. Always make sure that the primary borrower stays on top of payments and is someone you can trust.

Does paying off a loan early hurt my credit score?

Paying off a loan early may or may not hurt your credit score, in that paying it off too early could shorten your credit history and reduce your credit mix. Just as long as you focus on making on-time payments every month and keep your credit utilization at 30% (preferably 10% or below), then you should be in good shape.

Conclusion

All in all, following a smart and thoughtful approach will benefit you as you work towards increasing your credit score in 2025. By recognizing all of the changes to the scoring algorithms, understanding alternative scoring models, learning how AI factors into the mix, and having an entire picture of credit scoring as we move forward, you’ll be in a better position to take your score up to 750 and beyond in no time.

Best Loans is Alaska

Best Loans is Alaska