Alabama’s Consumer Credit Act – enforced by the State Banking Department – is designed to control the cost of installment loans and protect Alabama residents. The act limits the annual interest rate lenders can charge. It works like this: $15 per $100 on the first $750 you borrow and $10 per $100 for amounts exceeding $750 but less than $2,000. If you happen to default on the loan, you’re allowed a 10-day grace period to come up with the funds. After 10 days, the lender can impose a late payment fee of $18 or 5% of the default amount. However, the late payment fee cannot exceed $100.

For loans of $300,000 or more, the maximum repayment term is 36 months and 15 days. For loans less than $300,000, the maximum repayment term is 25 months and 15 days.

For smaller loans, lenders must abide by Alabama’s Small Loan Act. The legislation limits interest charges to 3% per month for loans less than $200 and 2% per month for loans between $200 to $1,000. Similarly, late payment fees cannot exceed $18 or 5% of the amount in default, but the maximum repayment term is 12 months.

When breaking down both documents, we found some overlap between the two statues. It isn’t entirely clear which act loans in the $751 to $1,000 range must abide by. Thus, before taking out an installment loan, make sure you ask the lender which regulation the loan falls under.

Loan Limit: You must wait one business day after repaying two consecutive loans

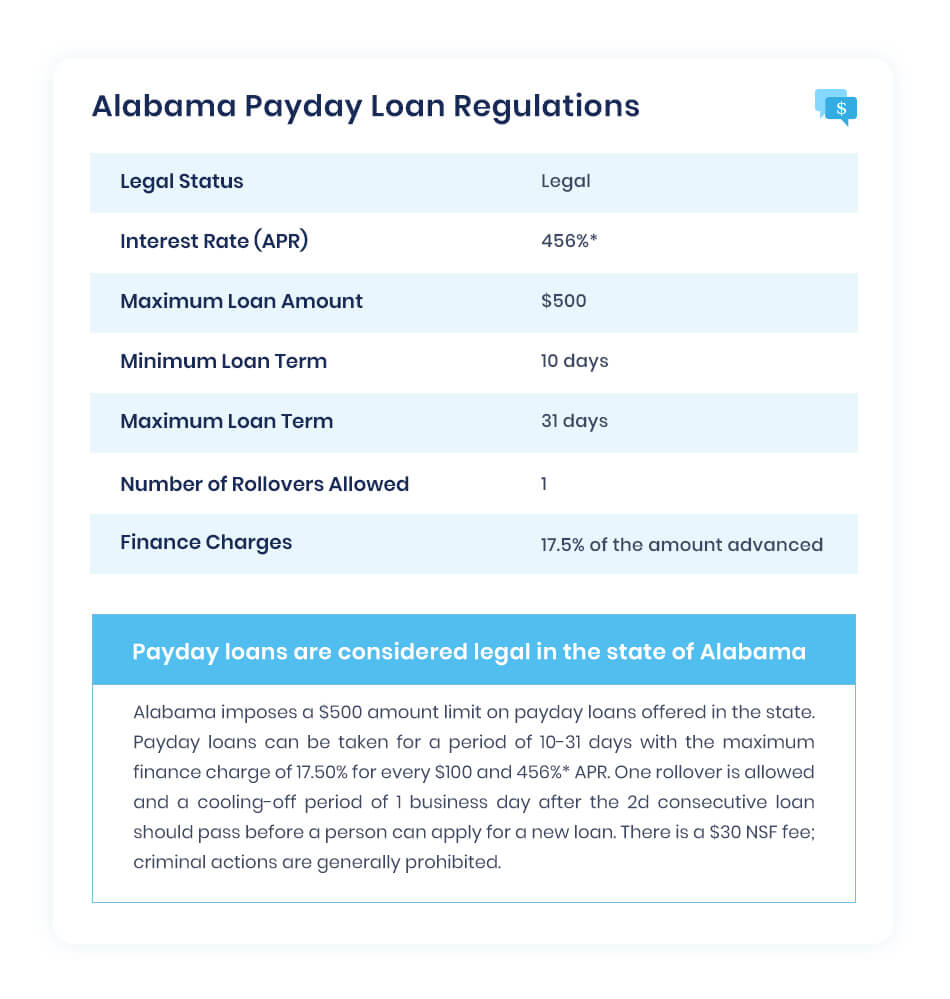

Payday loans are legal in Alabama. However, state law limits borrowing amounts to $500 and caps APRs at just over 456%. You’re allowed one rollover per loan, but after repaying your second consecutive payday loan, you must wait for at least one business before submitting another application. As well, lenders are allowed to charge a $30 non-sufficient funds fee.

Payday lenders are licensed under Alabama’s Deferred Presentment Services Act, Section-5-18A-1. All lenders must have a current license to comply and disclose all material information – including interest and fees – before a loan is officially processed. They’re also required to pay an annual license fee of $500 for each branch, office, or place of business that the lender operates.

Payday Loan Laws in Alabama by Country of April 2024

ElitePersonalFinance analysis of payday loan laws by countries in the State of Alabama.

We haven’t found a significant difference between the payday loan laws in Alabama. If you are with bad credit, here are the laws in Alabama by country.

City:

Amount Allowed:

APR Allowed:

Status:

Birmingham

$500

456%

Legal

Montgomery

$500

456%

Legal

Huntsville

$500

456%

Legal

Mobile

$500

456%

Legal

Tuscaloosa

$500

456%

Legal

Hoover

$500

456%

Legal

Dothan

$500

456%

Legal

Auburn

$500

456%

Legal

Decatur

$500

456%

Legal

Madison

$500

456%

Legal

Florence

$500

456%

Legal

Phenix City

$500

456%

Legal

Prattville

$500

456%

Legal

Gadsden

$500

456%

Legal

Vestavia Hills

$500

456%

Legal

Alabaster

$500

456%

Legal

Opelika

$500

456%

Legal

Enterprise

$500

456%

Legal

Bessemer

$500

456%

Legal

Homewood

$500

456%

Legal

Northport

$500

456%

Legal

Daphne

$500

456%

Legal

Athens

$500

456%

Legal

Pelham

$500

456%

Legal

Prichard

$500

456%

Legal

Anniston

$500

456%

Legal

Trussville

$500

456%

Legal

Albertville

$500

456%

Legal

Oxford

$500

456%

Legal

Mountain Brook

$500

456%

Legal

Fairhope

$500

456%

Legal

Troy

$500

456%

Legal

Selma

$500

456%

Legal

Helena

$500

456%

Legal

Foley

$500

456%

Legal

Tillmans Corner

$500

456%

Legal

Center Point

$500

456%

Legal

Talladega

$500

456%

Legal

Hueytown

$500

456%

Legal

Cullman

$500

456%

Legal

Millbrook

$500

456%

Legal

Alexander City

$500

456%

Legal

Scottsboro

$500

456%

Legal

Ozark

$500

456%

Legal

Hartselle

$500

456%

Legal

Saraland

$500

456%

Legal

Fort Payne

$500

456%

Legal

Gardendale

$500

456%

Legal

Muscle Shoals

$500

456%

Legal

Jasper

$500

456%

Legal

Pell City

$500

456%

Legal

Calera

$500

456%

Legal

Moody

$500

456%

Legal

Jacksonville

$500

456%

Legal

Chelsea

$500

456%

Legal

Irondale

$500

456%

Legal

Sylacauga

$500

456%

Legal

Leeds

$500

456%

Legal

Eufaula

$500

456%

Legal

Gulf Shores

$500

456%

Legal

Fairfield

$500

456%

Legal

Saks

$500

456%

Legal

Pleasant Grove

$500

456%

Legal

Atmore

$500

456%

Legal

Russellville

$500

456%

Legal

Clay

$500

456%

Legal

Rainbow City

$500

456%

Legal

Boaz

$500

456%

Legal

Meadowbrook

$500

456%

Legal

Valley

$500

456%

Legal

Forestdale

$500

456%

Legal

Fultondale

$500

456%

Legal

Bay Minette

$500

456%

Legal

Sheffield

$500

456%

Legal

Pike Road

$500

456%

Legal

Andalusia

$500

456%

Legal

Southside

$500

456%

Legal

Clanton

$500

456%

Legal

Tuskegee

$500

456%

Legal

Tuscumbia

$500

456%

Legal

Guntersville

$500

456%

Legal

Spanish Fort

$500

456%

Legal

Arab

$500

456%

Legal

Wetumpka

$500

456%

Legal

Greenville

$500

456%

Legal

Pinson

$500

456%

Legal

Brook Highland

$500

456%

Legal

Demopolis

$500

456%

Legal

Moores Mill

$500

456%

Legal

Hamilton

$500

456%

Legal

Montevallo

$500

456%

Legal

Meridianville

$500

456%

Legal

Lincoln

$500

456%

Legal

Oneonta

$500

456%

Legal

Robertsdale

$500

456%

Legal

Opp

$500

456%

Legal

Theodore

$500

456%

Legal

Lanett

$500

456%

Legal

Tarrant

$500

456%

Legal

Satsuma

$500

456%

Legal

Monroeville

$500

456%

Legal

Grayson Valley

$500

456%

Legal

Roanoke

$500

456%

Legal

Orange Beach

$500

456%

Legal

Attalla

$500

456%

Legal

Chickasaw

$500

456%

Legal

Harvest

$500

456%

Legal

Highland Lakes

$500

456%

Legal

Smiths Station

$500

456%

Legal

Brewton

$500

456%

Legal

Midfield

$500

456%

Legal

Fort Rucker

$500

456%

Legal

Glencoe

$500

456%

Legal

Daleville

$500

456%

Legal

Rainsville

$500

456%

Legal

Tallassee

$500

456%

Legal

Childersburg

$500

456%

Legal

Semmes

$500

456%

Legal

Jackson

$500

456%

Legal

Brent

$500

456%

Legal

Margaret

$500

456%

Legal

Headland

$500

456%

Legal

Piedmont

$500

456%

Legal

Pine Level

$500

456%

Legal

Winfield

$500

456%

Legal

Columbiana

$500

456%

Legal

Fayette

$500

456%

Legal

Geneva

$500

456%

Legal

Adamsville

$500

456%

Legal

Hokes Bluff

$500

456%

Legal

Redland

$500

456%

Legal

Argo

$500

456%

Legal

Springville

$500

456%

Legal

Holt

$500

456%

Legal

Holtville

$500

456%

Legal

Grand Bay

$500

456%

Legal

Mount Olive CDP

$500

456%

Legal

Alexandria

$500

456%

Legal

Thomasville

$500

456%

Legal

Haleyville

$500

456%

Legal

Citronelle

$500

456%

Legal

Elba

$500

456%

Legal

Valley Grande

$500

456%

Legal

Odenville

$500

456%

Legal

Evergreen

$500

456%

Legal

Union Springs

$500

456%

Legal

Centre

$500

456%

Legal

Cottondale

$500

456%

Legal

Hazel Green

$500

456%

Legal

Heflin

$500

456%

Legal

Ladonia

$500

456%

Legal

Livingston

$500

456%

Legal

Marion

$500

456%

Legal

West End-Cobb Town

$500

456%

Legal

Hanceville

$500

456%

Legal

Priceville

$500

456%

Legal

Moulton

$500

456%

Legal

Warrior

$500

456%

Legal

Emerald Mountain

$500

456%

Legal

Underwood-Petersville

$500

456%

Legal

Dadeville

$500

456%

Legal

Red Bay

$500

456%

Legal

York

$500

456%

Legal

Weaver

$500

456%

Legal

Kimberly

$500

456%

Legal

Lake View

$500

456%

Legal

What if I Don’t Qualify for a Loan?

If you’re struggling to obtain a loan, there are other ways to make money and bridge the gap. Today’s digital economy offers plenty of ways to earn extra cash and keep your finances above water. Some options include: working as an Uber driver, filling out paid surveys, or freelancing online. Whatever your preference, you can find helpful tips in our money-making guide.

Car Title Loans in Alabama of April 2024

Car title loans are also legal in Alabama.

But before choosing a lender, make sure the company is licensed in the state. Like payday lenders, car title lenders must pay an annual fee to maintain their license.

There are no limits on the amount you can borrow, and APRs can reach as high as 300% in Alabama. But because car title lenders are subject to Alabama’s Pawn Shop Act, loans have a maximum 30-day repayment period, and interest rates are capped at 25% per month.

What separates Alabama from other U.S. states is its repossession laws. If you default on the loan, a 30-day rollover begins. Here, you’re charged additional fees and interest, which are added to your original loan. If you’re still in default after the 30-day extension, the lender can repossess your car. But after the repossession and sale, Alabama state law allows lenders to keep any surplus profits from the transaction. For example, if you borrow $2,000 and your car is repossessed and sold for $3,500, the lender is legally allowed to keep the entire $3,500. Other U.S. states require the lender to return the $1,500 excess.

Alternative Payday Loans in Alabama of April 2024

If you don’t qualify for a personal loan, alternative payday loans are the next best thing. While their APRs are much higher than personal loans – ranging from 35.99% to roughly 200% – they’re a much cheaper option than traditional payday loans.

OppLoans is a prime example. The company’s APRs range from 59% to 160%, but the lender is licensed in Alabama and complies with all applicable laws. The State Banking Department granted its license.

For more information on how alternative lenders can help when others can’t, see our detailed guide.

Best Auto Loans for Bad Credit in Alabama of April 2024

Redstone Signature Loans allow you to borrow up to $5,000 and have fixed APRs that range from 10.25% to 18%. If you opt for a variable rate, you can receive an APR as low as 9.92%. Loans are unsecured, so no collateral is required. Redstone also offers a secured loan option where you use your savings account, certificate of deposit (CD), or annuity as collateral for the loan. By putting up collateral, you’re able to decrease your APR and still earn dividends on your collateral balance. Keep in mind that you need to be a member. To qualify, you must open a Redstone Savings Account and maintain a minimum balance of $5.

Redstone personal loans are available at 20 locations across Alabama, and the lender has branches in Huntsville, Hartselle, Arab, Guntersville, and many others.

America’s First Federal Credit Union

While loan amounts vary by the borrower, America’s First offers extremely competitive APRs. Personal loans have fixed APRs that range from 10.80% to 18%. You can also secure your loan and lower your APR. Like Redstone, you need to be a member to qualify. However, you only need to live, work, worship, or attend school in one of the following counties:

Bibb

Blount

Calhoun

Jefferson

Shelby

Clair

Walker

Mobile and Talladega (certain areas, not all)

America’s first also operates 19 branches across Alabama located in Bessemer, Cullman, Birmingham, Gardendale, etc.

MAX Credit Union

Offering unsecured loans that start at $1,000, MAX has APRs that range from 8.69% to 18%. You can also opt for a secured loan with APRs as low as 2% above your CD dividend rate.

All Licensed Credit Unions in Alabama of April 2024

Name:

City:

Size (Millions):

Members:

REDSTONE FEDERAL CREDIT UNION

Huntsville

$3,188.43

342640

AMERICA’S FIRST FEDERAL CREDIT UNION

Birmingham

$1,207.49

113174

MAX CREDIT UNION

Montgomery

$913.54

109921

ARMY AVIATION CENTER FEDERAL CREDIT UNION

Daleville

$1,033.24

105819

LISTERHILL EMPLOYEE’S CREDIT UNION

Sheffield

$540.80

69855

FAMILY SECURITY CREDIT UNION

Decatur

$462.04

67296

APCO EMPLOYEES CREDIT UNION

Birmingham

$2,129.51

63784

FAMILY SAVINGS FEDERAL CREDIT UNION

Gadsden

$281.04

58649

ALABAMA ONE CREDIT UNION

Tuscaloosa

$598.14

56986

ALABAMA TELCO CREDIT UNION

Birmingham

$573.11

54106

ALABAMA CREDIT UNION

Tuscaloosa

$479.31

46346

LEGACY COMMUNITY FEDERAL CREDIT UNION

Birmingham

$387.61

42358

COMMUNITY CREDIT UNION

Gadsden

$238.27

39765

MUTUAL SAVINGS CREDIT UNION

Birmingham

$161.29

37143

NEW HORIZONS CREDIT UNION

Mobile

$187.86

32699

AOD FEDERAL CREDIT UNION

Bynum

$228.91

30372

GUARDIAN CREDIT UNION

Montgomery

$212.08

30310

ALABAMA STATE EMPLOYEES CREDIT UNION

Montgomery

$195.37

27221

ALABAMA CENTRAL CREDIT UNION

Birmingham

$124.56

24627

COOSA PINES FEDERAL CREDIT UNION

Childersburg

$210.14

20608

FORT MCCLELLAN CREDIT UNION

Anniston

$167.03

20572

ALABAMA TEACHERS CREDIT UNION

Gadsden

$213.84

19482

AUBURN UNIVERSITY FEDERAL CREDIT UNION

Auburn

$134.10

17496

TVA CREDIT UNION

Muscle Shoals

$268.40

17474

FIRST EDUCATORS CREDIT UNION

Hoover

$117.23

16451

FIVE STAR CREDIT UNION

Dothan

$183.53

16137

MOBILE EDUCATORS CREDIT UNION

Mobile

$69.40

13617

ECO CREDIT UNION

Birmingham

$113.56

13591

NORTH ALABAMA EDUCATORS CREDIT UNION

Huntsville

$79.37

11580

SECURE FIRST CREDIT UNION

Birmingham

$46.72

10667

HERITAGE SOUTH CREDIT UNION

Sylacauga

$78.46

9651

UNIVERSITY OF SOUTH ALABAMA FEDERAL CREDIT UNION

Mobile

$30.24

8987

FOUR SEASONS FEDERAL CREDIT UNION

Opelika

$45.17

8825

JEFFERSON COUNTY EMPLOYEES CREDIT UNION

Birmingham

$65.54

8484

TUSCALOOSA TEACHERS CREDIT UNION

Tuscaloosa

$106.63

8463

ACIPCO FEDERAL CREDIT UNION

Birmingham

$134.82

7360

RIVERDALE CREDIT UNION

Selma

$48.82

7345

RAILROAD FEDERAL CREDIT UNION

Irondale

$107.40

6809

VALLEY CREDIT UNION

Tuscumbia

$60.48

6426

NAHEOLA CREDIT UNION

Pennington

$72.71

6109

DCH CREDIT UNION

Tuscaloosa

$32.45

5998

IAM COMMUNITY FEDERAL CREDIT UNION

Daleville

$37.44

5945

TUSCALOOSA CREDIT UNION

Tuscaloosa

$53.50

5761

WIREGRASS FEDERAL CREDIT UNION

Dothan

$39.33

5751

TUSCALOOSA V A FEDERAL CREDIT UNION

Tuscaloosa

$45.60

5562

GULF COAST FEDERAL CREDIT UNION

Mobile

$29.15

5255

CRAIG CREDIT UNION

Selma

$10.85

5137

TRI-RIVERS FEDERAL CREDIT UNION (TRFCU)

Montgomery

$18.45

5058

LANDMARK CREDIT UNION

Fairfield

$55.20

4832

THE INFIRMARY FEDERAL CREDIT UNION

Mobile

$14.00

4764

WOLVERINE CREDIT UNION

Decatur

$22.80

4743

ROCKET CITY FEDERAL CREDIT UNION

Huntsville

$39.00

4540

FLORENCE FEDERAL CREDIT UNION

Florence

$45.88

4393

EAST ALABAMA COMMUNITY FEDERAL CREDIT UNION (EAMCFCU)

Opelika

$10.19

4198

CHATTAHOOCHEE FEDERAL CREDIT UNION

Adamsville

$14.07

3785

ALABAMA RURAL ELECTRIC FEDERAL CREDIT UNION

Montgomery

$27.34

3658

SOCIAL SECURITY CREDIT UNION

Birmingham

$27.02

3634

BALDWIN COUNTY FEDERAL CREDIT UNION

Bay Minette

$18.21

3451

CHAMPION COMMUNITY CREDIT UNION

Courtland

$50.33

3130

AZALEA CITY CREDIT UNION

Mobile

$19.07

2954

MILESTONE CREDIT UNION

Fultondale

$20.58

2928

CITY CREDIT UNION

Tuscaloosa

$14.42

2726

SHORELINE CREDIT UNION

Mobile

$7.82

2673

LAUDERDALE COUNTY TEACHERS CREDIT UNION

Florence

$29.41

2521

ENERGEN CREDIT UNION

Birmingham

$20.12

2463

ELECTRICAL WORKERS NO 558 FEDERAL CREDIT UNION

Sheffield

$20.21

2446

OPP-MICOLAS CREDIT UNION

Opp

$12.97

2263

TUSKEGEE FEDERAL CREDIT UNION

Tuskegee

$5.01

2240

PIKE TEACHERS CREDIT UNION

Troy

$7.90

2229

BREWTON MILL FEDERAL CREDIT UNION

Brewton

$17.93

2018

ALLIED CREDIT UNION

Jackson

$13.22

2002

MCINTOSH CHEMICAL FEDERAL CREDIT UNION

Mcintosh

$17.95

1999

ANG FEDERAL CREDIT UNION

Birmingham

$19.55

1931

COVINGTON SCHOOLS FEDERAL CREDIT UNION

Andalusia

$16.64

1856

FEDMONT FEDERAL CREDIT UNION

Montgomery

$11.59

1850

STEVENSON FEDERAL CREDIT UNION

Stevenson

$16.02

1834

HEALTH CREDIT UNION

Birmingham

$20.77

1831

CITY OF B’HAM GENERAL EMPLOYEES CREDIT UNION

Birmingham

$5.75

1797

RAILWAY EMPLOYEES CREDIT UNION

Muscle Shoals

$16.87

1752

EBSCO FEDERAL CREDIT UNION

Birmingham

$13.34

1750

MONTGOMERY VA FEDERAL CREDIT UNION

Montgomery

$7.74

1748

BIRMINGHAM POLICE CREDIT UNION

Birmingham

$5.40

1699

TUSCALOOSA COUNTY CREDIT UNION

Tuscaloosa

$8.62

1651

MEAD COATED BOARD FEDERAL CREDIT UNION

Phenix City

$44.86

1574

MOBILE POSTAL CREDIT UNION

Mobile

$10.81

1530

ALABAMA RIVER CREDIT UNION

Monroeville

$14.15

1488

FEDERAL EMPLOYEES CREDIT UNION

Birmingham

$12.35

1488

PHENIX PRIDE FEDERAL CREDIT UNION (PPFCU)

Phenix City

$5.03

1381

L&N EMPLOYEES CREDIT UNION

Birmingham

$10.73

1343

MONROE EDUCATION EMPLOYEES FEDERAL CREDIT UNION

Monroeville

$4.31

1302

PEOPLE’S FIRST FEDERAL CREDIT UNION

Tarrant

$5.74

1200

NORTHEAST ALABAMA POSTAL FEDERAL CREDIT UNION

Anniston

$14.41

1180

MOBILE GOVERNMENT EMP. CREDIT UNION

Mobile

$22.18

1152

ANDALUSIA MILLS EMPLOYEES CREDIT AS FEDERAL CREDIT UNION

Andalusia

$2.76

1082

SYCAMORE FEDERAL CREDIT UNION

Sycamore

$10.81

1078

O’NEAL CREDIT UNION

Birmingham

$2.66

1074

MARVEL CITY FEDERAL CREDIT UNION

Bessemer

$7.66

1026

SIXTH AVENUE BAPTIST FEDERAL CREDIT UNION

Birmingham

$4.38

989

COUNCILL FEDERAL CREDIT UNION

Huntsville

$2.95

944

N.E.A.R.M.C. EMPLOYEES FEDERAL CREDIT UNION

Anniston

$3.25

941

BLUE FLAME CREDIT UNION

Mobile

$7.89

907

PROGRESSIVE FEDERAL CREDIT UNION

Mobile

$6.19

894

DEGUSSA EMPLOYEES FEDERAL CREDIT UNION

Theodore

$5.69

871

NEW PILGRIM FEDERAL CREDIT UNION

Birmingham

$1.53

853

FIREMAN’S CREDIT UNION

Birmingham

$3.91

838

ALABAMA POSTAL CREDIT UNION

Birmingham

$6.80

811

BRASSIES CREDIT UNION

Anniston

$8.26

749

TVH FEDERAL CREDIT UNION

Tuskegee

$4.43

732

CLARKE EDUCATORS FEDERAL CREDIT UNION

Auburn

$2.72

729

DEMOPOLIS FEDERAL CREDIT UNION

Demopolis

$0.54

672

U S PIPE BESSEMER EMPLOYEES FEDERAL CREDIT UNION

Bessemer

$3.06

586

FOGCE FEDERAL CREDIT UNION

Eutaw

$1.19

570

NUCOR EMPLOYEES FEDERAL CREDIT UNION

Fort Payne

$3.48

450

DIXIE CRAFT EMPLOYEES CREDIT UNION

Goodwater

$2.72

441

CHEMCO CREDIT UNION

Mcintosh

$4.63

418

NORTH ALABAMA PAPERMAKERS FEDERAL CREDIT UNION

Stevenson

$1.90

411

S R I EMPLOYEES FEDERAL CREDIT UNION

Birmingham

$6.91

409

POSTAL EMPLOYEES CREDIT UNION

Huntsville

$3.23

384

NRS COMMUNITY DEVELOPMENT FEDERAL CREDIT UNION

Birmingham

$0.98

359

CHEM FAMILY CREDIT UNION

Anniston

$6.33

323

TUSCUMBIA FEDERAL CREDIT UNION

Tuscumbia

$1.44

287

ST. JOHNS AME BIRMINGHAM FEDERAL CREDIT UNION

Birmingham

$0.05

204

EMPLOYEES SAVINGS CREDIT UNION

Montgomery

$2.54

203

FIRST KINGDOM COMMUNITY FEDERAL CREDIT UNION

Selma

$0.15

109

Student Loans in Alabama of April 2024

If you need a loan to help pay for college, Federal student loans – obtained through the U.S. Department of education – are the most common. Federal student loans are preferable to private student loans because they offer debt forgiveness, charge zero interest until you graduate, and allow you to repay the proceeds as a percentage of your income. For more information, see our detailed guide.

At the state level, though, Alabama residents have access to grants and subsidy programs designed to make college more affordable.

Alabama Student Assistance Program (ASAP)

The ASAP Program provides anywhere from $300 to $5,000 in funding per year to students in need of financial aid. To be eligible, you must be a resident of Alabama and attend one of the 80 partner institutions. As well, you need to submit your application by October 1st of each year. You can do so through the Federal Student Aid website or your prospective school’s financial aid office.

Alabama Student Grant Program

Unlike the ASAP, the Alabama Student Grant Program is determined by academic merit and not financial need. The amount you qualify for varies, but funding never exceeds $1,200 per year. Only select institutions participate in the program, but here is the list of eligible colleges and universities:

Amridge University

Birmingham Southern College

Faulkner University

Huntingdon College

Judson College

Miles College

Oakwood University

Samford University

Spring Hill College

South University – Montgomery

Stillman College

S. Sports Academy

University of Mobile

Federal Housing Administration (FHA) Loans in Alabama of April 2024

FHA loans are used to help middle and low-income families achieve their dream of owning a home. They require a small down payment and have lower credit score requirements. In Alabama, you also have the option to refinance up to 97.5% of your home’s value or cash out up to 85% of its value.

Eligibility requirements include:

A 3.5% down payment on your property.

The home must be your primary residence.

If you filed for Chapter 7 bankruptcy, you must wait 2 years (after your bankruptcy was charged off) before applying for an FHA loan.

If your home was foreclosed, you must wait 3 years before applying for an FHA loan.

Like many states across the U.S., FHA loan limits vary by county and the size of the property.

Here are the figures by county:

County:

Single Unit Limit (lowest):

Four-Plex Limit (highest):

Autauga County

$331,760

$638,100

Baldwin County

$331,760

$638,100

Barbour County

$331,760

$638,100

Bibb County

$331,760

$638,100

Blount County

$331,760

$638,100

Bullock County

$331,760

$638,100

Butler County

$331,760

$638,100

Calhoun County

$331,760

$638,100

Chambers County

$331,760

$638,100

Cherokee County

$331,760

$638,100

Chilton County

$331,760

$638,100

Choctaw County

$331,760

$638,100

Clarke County

$331,760

$638,100

Clay County

$331,760

$638,100

Cleburne County

$331,760

$638,100

Coffee County

$331,760

$638,100

Colbert County

$331,760

$638,100

Conecuh County

$331,760

$638,100

Coosa County

$331,760

$638,100

Covington County

$331,760

$638,100

Crenshaw County

$331,760

$638,100

Cullman County

$331,760

$638,100

Dale County

$331,760

$638,100

Dallas County

$331,760

$638,100

Dekalb County

$331,760

$638,100

Elmore County

$331,760

$638,100

Escambia County

$331,760

$638,100

Etowah County

$331,760

$638,100

Fayette County

$331,760

$638,100

Franklin County

$331,760

$638,100

Geneva County

$331,760

$638,100

Greene County

$331,760

$638,100

Hale County

$331,760

$638,100

Henry County

$331,760

$638,100

Houston County

$331,760

$638,100

Jackson County

$331,760

$638,100

Jefferson County

$331,760

$638,100

Lamar County

$331,760

$638,100

Lauderdale County

$331,760

$638,100

Lawrence County

$331,760

$638,100

Lee County

$331,760

$638,100

Limestone County

$331,760

$638,100

Lowndes County

$331,760

$638,100

Macon County

$331,760

$638,100

Madison County

$331,760

$638,100

Marengo County

$331,760

$638,100

Marion County

$331,760

$638,100

Marshall County

$331,760

$638,100

Mobile County

$331,760

$638,100

Monroe County

$331,760

$638,100

Montgomery County

$331,760

$638,100

Morgan County

$331,760

$638,100

Perry County

$331,760

$638,100

Pickens County

$331,760

$638,100

Pike County

$331,760

$638,100

Randolph County

$331,760

$638,100

Russell County

$331,760

$638,100

Shelby County

$331,760

$638,100

St. Clair County

$331,760

$638,100

Sumter County

$331,760

$638,100

Talladega County

$331,760

$638,100

Tallapoosa County

$331,760

$638,100

Tuscaloosa County

$331,760

$638,100

Walker County

$331,760

$638,100

Washington County

$331,760

$638,100

Wilcox County

$331,760

$638,100

Winston County

$331,760

$638,100

Business Loans in Alabama of April 2024

As you can see, loan limits remain fairly constant throughout each county. The lowest FHA loan amount is $314,827, while the highest is $636,900. Only three counties in Alabama – Hale, Pickens, and Tuscaloosa – allow for higher borrowing amounts than the rest of the state.

If you need a business loan, these online lenders offer reliable service and extremely competitive APRs:

However, if you don’t qualify for the options above or prefer to deal with a local lender in Alabama, the options below are a solid alternative.

LiftFund Loans

While the company doesn’t disclose its APRs, LiftFund is a non-profit lender that offers as little as $500 to upwards of $1,000,000. Loans are available to business owners in Birmingham, Mobile, Tuscaloosa, Montgomery, and Huntsville. The average credit score of LiftFund borrowers is 575 – much lower than traditional banks. As well, if your credit score is less than 575, there is a co-signer option.

All businesses qualify for LiftFund loans except those in the adult entertainment industry. However, if you filed for Chapter 7 bankruptcy in the last two years or Chapter 12 bankruptcy in the last year, you’re ineligible.

There is a wide range of banks and credit unions in Alabama that offer in-state business loans. Reputable lenders include the First Bank of Alabama, Peoples Bank of Alabama, and the Alabama Credit Union. However, loan amounts and APRs vary depending on your business needs and your company’s cash flows. When deciding between lenders, it’s best to set up an in-house consultation and discuss your options.

How to Avoid Debt Cycle

When bills are piling up, taking out a loan can seem like your only option. However, if you’re not careful, the process can quickly get out of hand. You end up trying to service several loans that continue to compound with interest.

If you’re struggling and not sure where to turn, consider contacting a credit counselor. They can advise you on how to reduce your debt load and work with creditors to find an amicable solution. Many are available through non-profit organizations, and you can find help through the National Foundation for Credit Counseling.

Through the CFPB’s website, you can also find information on developing a debt management plan and avoiding upfront fees when working with debt settlement companies.

Conclusion

If you’re a resident of Alabama and need a reliable loan, you’ve come to the right place. We found plenty of reputable lenders – both online and in-state – that provide affordable financing. When narrowing your search, we always recommend you start with personal loans. APRs are capped at 35.99% even for those with bad credit, so they remain a reliable option. As well, Alabama credit unions are another great alternative. Their APRs are capped at 18%, which makes them extremely affordable. However, before taking out any loan, determine whether the product is regulated by Alabama’s Consumer Credit Act or the Small Loan Act. There is a slight overlap between the two statutes, so it’s best to ask ahead of time to avoid surprises.

Best Loans is Alaska

Best Loans is Alaska